Between a Coverdell vs. 529 plan, which will grow money faster for my kid’s college fund?

As the cost of education continues to rise, setting up a plan to cover your child’s college tuition is becoming more and more important. When starting to save, the first decision many parents make is deciding between a Coverdell vs. 529 plan.

Both the 529 Plan and the Coverdell Education Savings Account (ESA) are popular because they offer tax-free growth for qualified education expenses, but they each have their own distinct features.

A 529 Plan is a state-sponsored education savings plan. When used for qualified education expenses, withdrawals are tax-free. Qualified expenses include things like tuition, fees, books, and room and board.

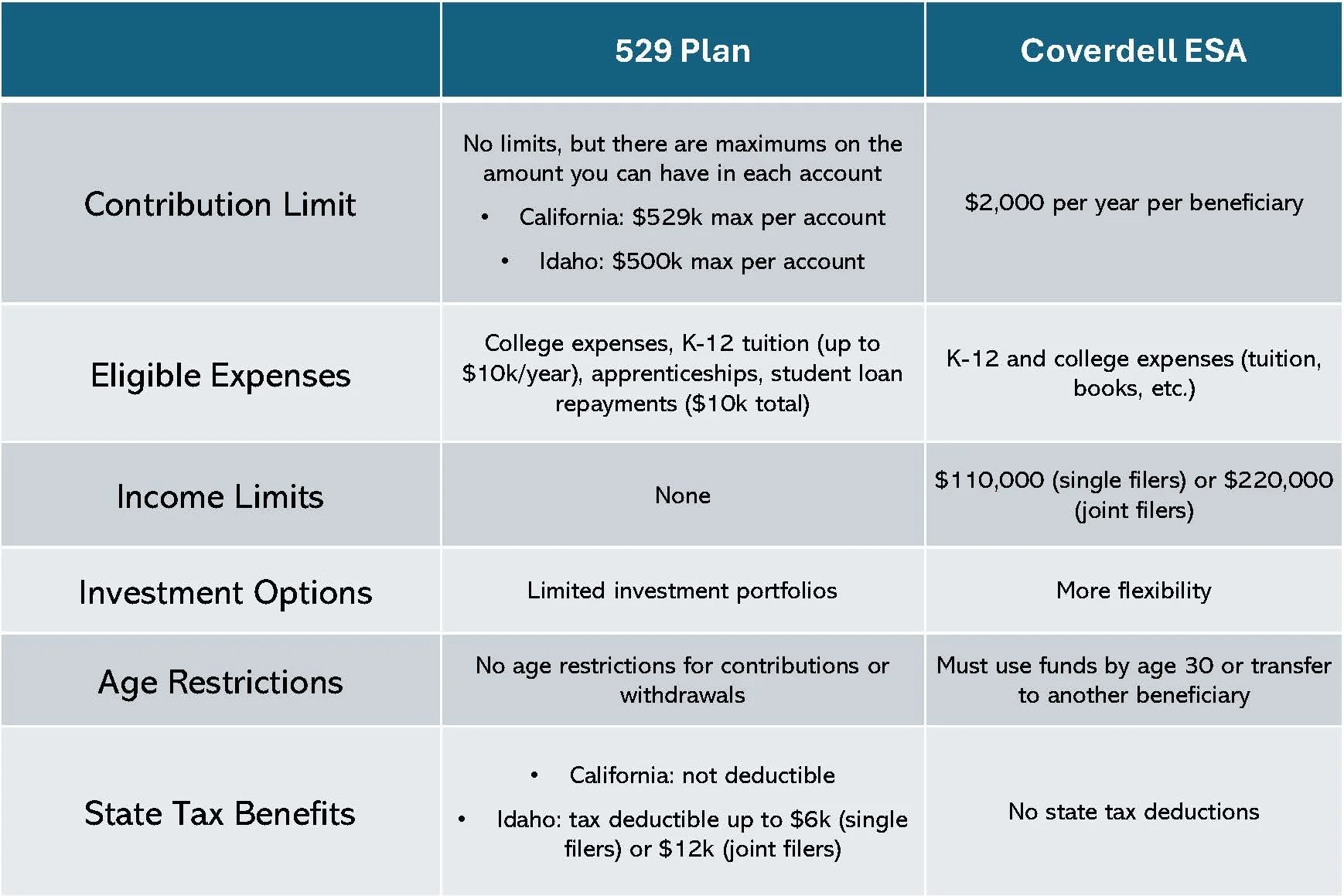

529s have no investment limit. Also, anyone can contribute to a 529 – there is no maximum income level you must fall under.

There are two types of 529 Plans: the Education Savings Plan and the Prepaid Tuition Plan.

Education Savings Plans are more common. You put money in which is then invested in a portfolio (you pick the portfolio, but the portfolios are built by the plan – you cannot choose individual stocks, funds, etc.). You can then use that money to pay for college expenses (unlimited), K-12 expenses (up to $10k annually), apprenticeships, or for student loan repayments (up to $10k total).

Prepaid tuition plans are less common. Like a regular 529, you invest money that grows tax-free. The difference is that they guarantee today’s tuition rate of a specific school. While guaranteeing today’s rate may seem ideal, they’re less common for two reasons. First, because only nine states offer them. Second, because they usually require you to guarantee that the funds will be used at a specific school. With non-guarantees on admission, this can be risky.

There are technically no contribution limits for a 529, but some states do have limits on the amount in your account. In California, that maximum is $529,000. In Idaho, the limit is $500,000.

Funds are federal and state income tax free (when used for qualifying education expenses). Using the money for other purposes subjects it to taxes and a 10% penalty (there are exceptions if you use the funds for reasons due to death or disability).

Sometimes it’s necessary to use the money for other things – maybe your child got a full ride or decided not to go to school. You could withdraw the money with the penalty, but 529s also allow for transfers to qualified relatives, and sometimes to a Roth IRA. (Roth IRA transfers must be from a 529 that is at least 15 years old).

In California, contributions to 529s are not tax-deductible. However, in Idaho, contributions are tax-deductible (up to $6000 for single filers and up to $12000 for joint filers).

The other popular college savings account is a Coverdell ESA.

There are two main differences between Coverdell vs 529. The first is that Coverdell ESAs have a maximum yearly contribution of $2000. Second, you can choose where to invest the money (not just into pre-determined investment portfolios).

Withdrawals are tax-free when they are less than the sum of all education expenses in a given year. If the withdrawal is more than that year’s expenses, they are taxed at the account holder’s normal income tax rate.

Another difference is that to contribute to a Coverdell ESA, you cannot exceed a certain income. If your income is over $110,000, you are ineligible. If you are married and file jointly, that maximum is $220,000.

Also, funds must be used by the time your child is 30 years old. If they don’t use it for education expenses, it will be taxed as normal income.

In both California and Idaho, contributions to Coverdell ESAs are not tax-deductible.

529s and Coverdell ESAs each have their own advantages and disadvantages.

A 529 may be a better option for you if you plan to contribute over $2000 per year, you have a high income, and are not picky about investment portfolios. A Coverdell ESA may be better for you if you want more investment control and plan to contribute less than $2000 annually.

As always, we recommend working with a tax professional who understands both tax strategies and wealth management.

Author: Rob Cucchiaro, CFP®, CRPC, AAMS

Questions answered in this article:

What is a 529 Plan?

What is a Coverdell ESA?

What are qualified educational expenses?

Are withdrawals tax-free with a 529?

What are the two types of 529 Plans?

What if I saved money in a 529 but my kid doesn’t go to college?

Does a 529 have contribution limits?

Do I need to fall under a certain AGI to set up a 529?

Does my 529 need to be used on college expenses?

What if my kid graduated from college and their 529 has leftover funds?

What is the maximum amount my 529 can have as a California resident?

What is the maximum amount my 529 can have as an Idaho resident?

Are 529 contributions tax deductible in Idaho?

Are 529 contributions tax deductible in California?

Does a Coverdell ESA have contribution limits?

What is the Coverdell contribution limit?

Are Coverdell contributions tax deductible in Idaho?

Are Coverdell contributions tax deductible in California?

Are withdrawals tax-free with a Coverdell?

What is the maximum income I can have and still contribute to a Coverdell in Idaho?

What is the maximum income I can have and still contribute to a Coverdell in California?

What if I have money leftover in a Coverdell after my kid finishes college?

What if I have money leftover in a Coverdell after I finish college?

Can I transfer a Coverdell ESA to another person?

What is the difference between a Coverdell vs 529?