Gifting Appreciated Assets to a Charitable Remainder Trust

Whether it’s individual stock, real estate, or a closely held family business, when a taxpayer is contemplating the sale of a highly appreciated asset, one of their primary questions is around what can be done to mitigate the tax bill.

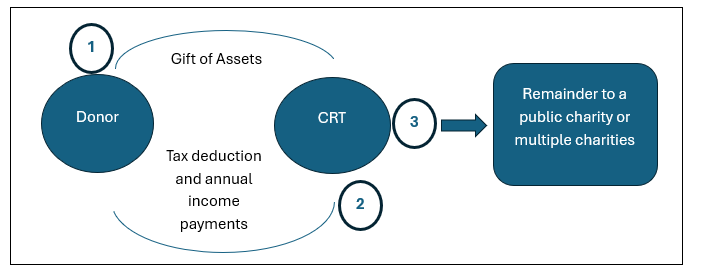

One of the strategies worth considering is a CRT, or charitable remainder trust.

A CRT is an irrevocable trust created by the donor (the person who owns the asset) during their lifetime. That person creates a trust and gifts the asset (or part of the asset) into the trust in exchange for what’s called a lead interest. The lead interest refers to the income they will receive from this trust and the period of time that income will cover; which can be anywhere from their lifetime or a term not to exceed 20 years.

CRTs can be extremely useful for a taxpayer who has a large capital gain and wants to both receive an upfront tax deduction and spread the tax bill over time, to reduce or avoid the net investment income tax (NIIT).

Benefits of a CRT

Variable or fixed income (CRAT vs. CRUT) payments to the donor each year

Upfront income tax deduction (the year the gift was made), which may be used all in one year or carried forward up to 5 additional years

Pay no immediate capital gains tax on the sale of the appreciated assets

Reduce or eliminate estate taxes owed on that asset

Diversify away from a concentrated asset

Make a gift to your favorite charity or multiple charities

Like all tax planning strategies, you need to understand the potential advantages and disadvantages. Before moving forward, it is vital to produce a personal 10-year cash flow report as a first step in the process.

As always, we recommend working with a tax professional who understands both tax strategies and wealth management.