Navigating 1031 Exchanges: Tax-Deferred Real Estate Investments

Imagine having the power to sell your investment property without the looming shadow of capital gains taxes, allowing you to reinvest the sale profits into your next opportunity. This is possible through a real estate investment strategy known as 1031 exchanges. By strategically navigating the ins and outs of this tax-deferral strategy, you can enhance your real estate portfolio while unlocking greater investment potential. Whether you’re a seasoned investor or just starting out, understanding 1031 exchanges could help you on the path towards your financial goals.

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, allows real estate investors to defer paying capital gains taxes on an investment property when it is sold, as long as another similar property is purchased with the profit gained by the sale. This process is often referred to as a "like-kind exchange."

While a “like-kind exchange” has a broad meaning, there are a few key stipulations regulating what falls under the umbrella of compliant 1031 exchanges. The properties exchanged must be held for investment purposes, which includes rental properties, commercial properties, and land. Personal residences or properties intended for personal use do not qualify. For instance, you could exchange a multi-family rental property for a commercial building, as both are considered real estate investments. Almost any real estate property can be considered like-kind to another as long as they are in the same asset class (real property). For example, a retail property can be exchanged for an apartment complex.

On the other side of the coin are non-like-kind property. Stocks, bonds, and personal property like artwork or machinery cannot be considered like-kind. However, it is possible that non-like-kind-property can be included in the sale of a property eligible for a 1031 exchange. This non-eligible property is referred to as “boot.” When boot is received in the exchange, that portion may be subject to taxation.

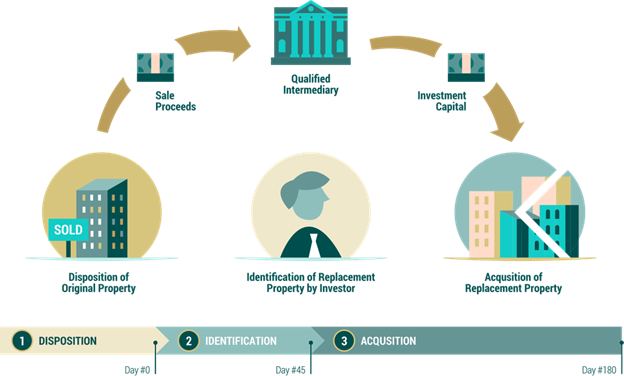

The fundamental premise of a 1031 exchange is that it enables investors to sell an investment property and reinvest the proceeds into a new property, deferring taxes on any gain. Broken down to the most simplified process, there are three necessary steps to go through during the process of a 1031 exchange.

First, the investor must identify the properties. The property being sold is known as the "relinquished property," while the new property is referred to as the "replacement property." The investor must identify potential replacement properties within 45 days of the sale of the relinquished property.

Second, the investor must use a qualified intermediary (QI). A Qualified Intermediary is a neutral third party who must facilitate the exchange process. Their role is to hold the funds from the sale of the relinquished property and ensure that the exchange complies with IRS regulations. Once a replacement property is identified (within 45 days of the original sale), the QI uses the held funds to purchase the new property on behalf of the investor (180 days to close). The QI’s role is vital because the investor cannot receive the sale proceeds directly without jeopardizing the tax-deferred status of the exchange. A QI can be anyone, but most commonly they are attorneys, accountants, or employees within specialized companies.

Last, the exchange must be completed. The replacement property must be acquired within 180 days of the sale of the relinquished property.

1031 exchanges may seem difficult to pull off, but they are extremely useful for tax strategy and wealth management if carried out correctly. While real estate professionals often see the most direct benefits from 1031 exchanges, a variety of other individuals and professionals can also gain significant advantages.

For example, investors and property owners may see their benefit in tax deferrals (reinvesting the full amount into new investment opportunities without immediate liability) and in portfolio diversification. Also, investors who focus on investments in Opportunity Zones can see additional benefits due to the potential tax breaks outlined in the Tax Cuts and Jobs Act of 2017. Through reinvestment in Opportunity Zone properties, investors can enhance their overall returns while contributing to community development.

Any individual with multi-generational planning goals can benefit from 1031 exchanges thanks to their relevance to estate planning. By deferring taxes, clients can keep more capital invested, potentially providing greater value for their family’s future generations. Also, when property is passed on to heirs, they may benefit from a stepped-up basis, potentially eliminating capital gains taxes altogether if structured properly. A stepped-up basis refers to the idea that if you inherit property, the tax basis for that property is "stepped up" to its current market value, rather than the value at which the deceased purchased it. For example, let’s say a parent purchases a house for $1 million. At the time of the parent's death, the fair market value of the house has increased to $2 million. The house is then inherited by their adult child, who decides to sell it shortly after. If they decide to sell the house for $2.5 million, here’s how the capital gains tax would be calculated: Selling Price: $2.5 million; Stepped-Up Basis: $2 million; Capital Gain: $2.5 million - $2 million = $500,000. So, the child would pay capital gains tax only on the $500,000 gain, rather than on the $1.5 million gain (which would have been calculated using the original purchase price of $1 million).

Commercial developers can also benefit from the reinvestment opportunities provided by 1031 exchanges. Developers can sell completed projects and reinvest the proceeds into new developments without the immediate tax burden, facilitating continuous growth and project expansion. Further, developers can use them for strategic property acquisition, purchasing properties that better fit their evolving business models, such as shifting from residential to commercial developments. And, an evolving business model such as that is still considered a “like-kind exchange.” Similarly, business owners can use 1031 exchanges to support their growth and operational needs. By selling and reinvesting in new real estate, used for their business, such as moving to a bigger location or to upgrade facilities, they can expand their business without incurring capital gains taxes.

Your financial planner and tax professionals must be knowledgeable and experienced with 1031 exchanges to implement them properly into your investment strategy, helping you to grow wealth more efficiently thanks to the tax deferral.

In investment management, 1031 exchanges can facilitate portfolio diversification and risk management. Reallocating investments is useful for investors with a wide range of long-term goals. For example, investors can use 1031 exchanges to move into different property types or geographic areas, reducing risk and optimizing returns. Utilizing 1031 exchanges aligns with a long-term investment strategy, allowing investors to grow their portfolio without immediate tax implications.

1031 exchanges play a significant role in tax planning. By deferring capital gains taxes, investors can preserve more capital for reinvestment. This strategy is particularly useful in high-growth areas where property values appreciate rapidly. Again, 1031 exchanges do not eliminate taxes, but they do allow for deferral. This can result in a larger capital base for future investments, leading to greater overall wealth accumulation.

Here’s a breakdown of what an investor might expect to pay in California, Idaho, and Washington, along with how much they could save with a 1031 exchange.

1. California

In California, capital gains are taxed as regular income. The state has a progressive income tax rate that ranges from 1% to 13.3%. For high-income earners, selling a property can lead to a substantial tax burden.

Example:

If you sell a property for $2 million, and your adjusted basis is $1 million, you have a $1 million capital gain.

Assuming you're in the highest tax bracket (13.3%), the state tax alone would be approximately $133,000.

Federal capital gains tax could add an additional 20% (if you fall under long-term capital gains), equating to $200,000

Total Tax Liability: Approximately $333,000.

Tax Savings: By using a 1031 exchange, you could defer this entire $333,000 in taxes, allowing you to reinvest the full $2 million into a new property.

2. Idaho

Capital Gains Tax Rate: Idaho taxes capital gains at a rate that matches its income tax rate, which is a flat 6.5%.

Example Calculation:

Selling a property for $1.5 million with an adjusted basis of $1 million results in a $500,000 gain.

The state tax would be about $32,500, while the federal tax would be around $100,000 (20%).

Total Tax Liability: Approximately $132,500.

Tax Savings: Utilizing a 1031 exchange would allow you to defer the $132,500 in capital gains taxes, providing more capital to reinvest.

3. Washington

Capital Gains Tax Rate: Washington state does not impose a capital gains tax on the sale of real estate. However, since the introduction of a new capital gains tax on high earners (7% on gains exceeding $250,000), it’s essential to consult a tax professional for specific implications.

Example:

For a property sold for $3 million with a basis of $1 million, the gain is $2 million.

If subject to the new tax, you would owe $122,500 on the gains over the threshold (7% on the $1.75 million).

Total Tax Liability: Approximately $122,500.

Tax Savings: With a 1031 exchange, you could defer this tax, maintaining more liquidity for future investments.

Using a 1031 exchange can yield significant tax savings, particularly in states with high capital gains taxes like California. The ability to defer taxes not only allows for a more substantial reinvestment but also optimizes long-term investment strategies. Understanding the mechanics behind 1031 exchanges and their specific tax implications based on location and individual circumstances is crucial for any investor looking to leverage this tool. As always, we recommend working with a tax professional who understands both tax strategies and wealth management.